Rich Old People

Key Takeaways

Analyze demographic data to understand consumer behavior and tailor strategies accordingly.

Educate younger clients on financial instruments like IRAs and 401(k)s to promote wealth accumulation.

Prepare for the impending wealth transfer by developing strategies that address the needs of inheriting generations.

Monitor housing market trends closely to anticipate shifts in supply and demand dynamics.

Engage in discussions about financial literacy to bridge the gap between generations.

The Problem: Wealth Disparity and Generational Frustration

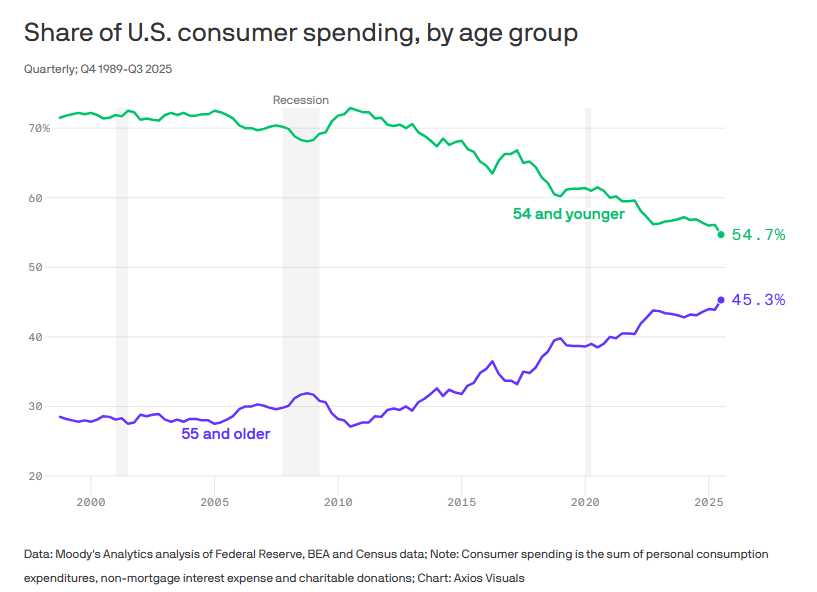

The economic landscape is increasingly characterized by a significant wealth disparity between older and younger generations. With individuals aged 55 and older accounting for over 45% of consumer spending and controlling nearly three-quarters of the nation's wealth, younger generations often feel frustrated and resentful. This sentiment is exacerbated by the challenges younger people face in achieving financial stability, such as high housing costs and stagnant wages. Understanding this dynamic is crucial for mid-level practitioners who must navigate these generational tensions in their professional environments.

Demographic Trends: The Rise of Older Adults

The aging population is a demographic trend that cannot be ignored. The baby boomer generation, the largest cohort in U.S. history, is living longer than previous generations, leading to an unprecedented number of older adults in the economy. According to Eric Finnigan from John Burns, this demographic shift is significant, as it alters the landscape of consumer behavior and wealth distribution. Practitioners should leverage demographic data to inform their strategies, ensuring they address the needs and preferences of both older and younger consumers.

Financial Assets: The Boomers' Wealth Accumulation

Baby boomers have benefited from several financial advantages, including access to IRAs and 401(k)s, which have allowed their wealth to compound over decades. Many have also paid off their mortgages, further increasing their net worth. This wealth accumulation is not merely a product of luck; it is the result of strategic financial planning and market conditions that favored long-term investment. Mid-level practitioners should study these financial instruments and consider how similar strategies can be applied to younger generations, who may not have the same opportunities.

The Inheritance Factor: Future Wealth Transfer

As the older generation passes away, a significant transfer of wealth is expected. Estimates suggest that Gen Xers and Millennials will inherit approximately $4.6 trillion in global real estate over the next decade, with nearly half of that in the U.S. This impending wealth transfer presents both opportunities and challenges for the housing market. Practitioners should prepare for shifts in market dynamics as younger generations inherit properties, potentially leading to increased supply in the housing market.

Implications for the Housing Market

The question remains: how will younger generations respond to inherited properties? Will they sell, occupy, or rent these homes? Understanding these potential behaviors is critical for real estate professionals and financial advisors. The concept of a Silver Tsunami—a large influx of homes coming to market due to aging homeowners—could reshape the housing landscape. Practitioners should develop strategies that account for these shifts, such as targeting younger buyers and adapting to changing market conditions.

Why it matters

Understanding the economic impact of an aging population will enhance your ability to navigate generational tensions in the workplace. By applying these insights, you can develop strategies that resonate with both older and younger clients, ultimately fostering better relationships and driving business success.

Get your personalized feed

Trace curates the best articles, videos, and discussions based on your interests and role. Stop doom-scrolling, start learning.

Try Trace free