Can You Live Off Your Dividends?

Key Takeaways

A 4% withdrawal rate requires a portfolio of $4.25M to sustain an annual income of $170k.

Covered call strategies can provide income but may limit upside potential in bull markets.

Consider total return, not just yield, when evaluating investment strategies.

Inflation poses a significant risk for those relying solely on dividend income.

At 42, with $2M in assets, options include reducing spending, selling the business, or taking a break to reassess life goals.

The Financial Situation

A reader presents a financial scenario with $1.6 million in a taxable brokerage account, $250,000 in a traditional 401k, and $150,000 in cash, totaling $2 million in assets. With no debt and a need for $170,000 in annual income to retire, the reader faces a challenge. To sustain this income with a traditional 4% withdrawal rate, they would need a portfolio of $4.25 million. This stark reality sets the stage for exploring alternative income strategies, such as covered call funds, which have gained popularity recently.

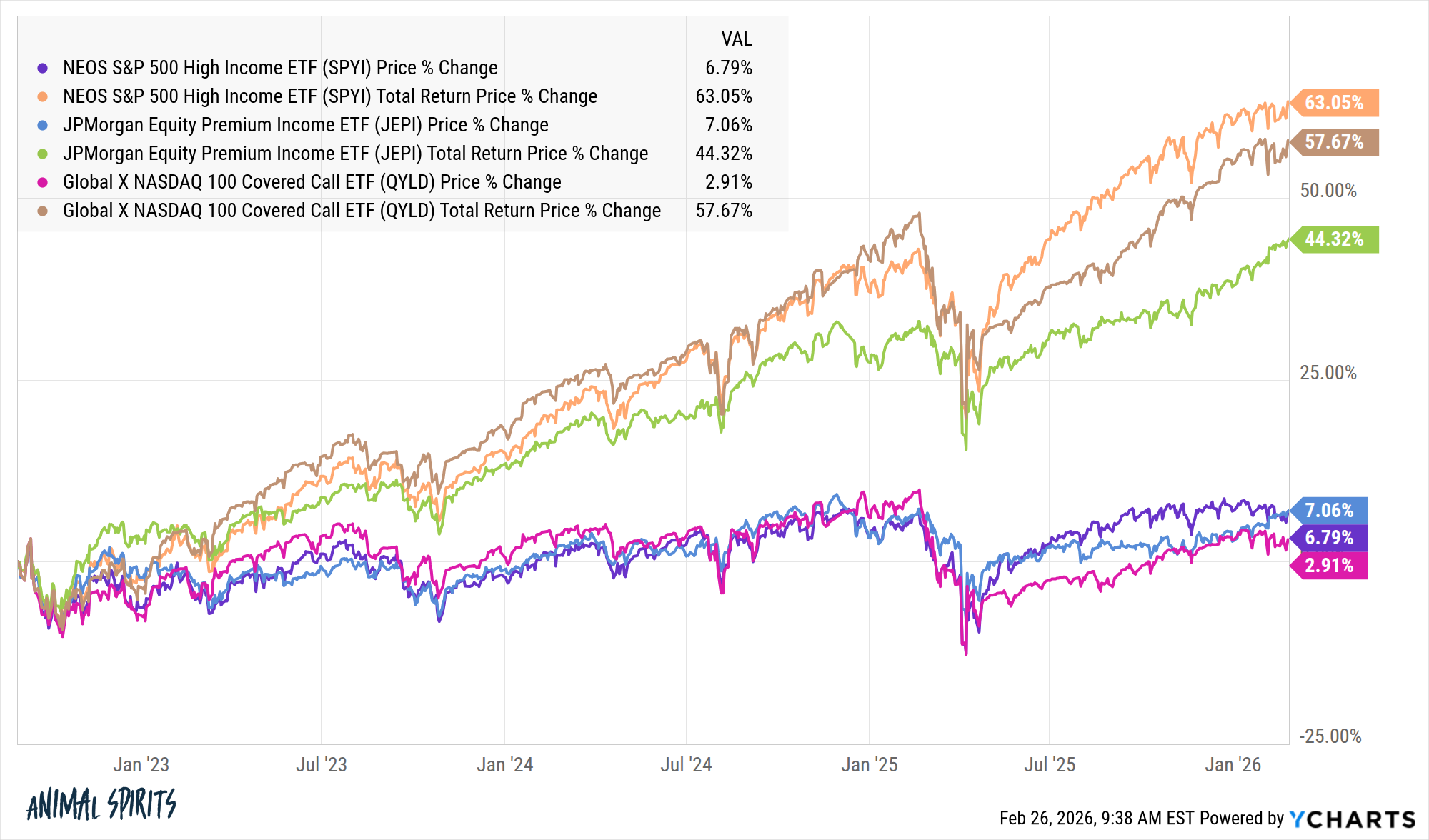

Understanding Covered Call Strategies

Covered call strategies involve selling call options on stocks or indices you own. A call option gives the buyer the right to purchase a security at a predetermined price. If the stock does not reach this price, the seller retains the premium. For instance, if you own shares worth $1,000 and sell call options, you might earn a yield of 2.5%. However, this strategy limits potential gains if the stock price exceeds the strike price. In a bull market, this could lead to underperformance compared to the overall market, while in a bear market, the income from options can provide a buffer against losses.

The Risks of High-Yield Investments

The allure of high yields from covered call funds, especially after the 2022 bear market, must be approached with caution. While these funds can outperform in downturns, the yield should not be mistaken for a guaranteed income. The total return, which includes price appreciation, is crucial. Many covered call strategies have shown minimal price returns, indicating that the income generated is the primary source of return. Relying solely on yield can expose investors to inflation risk, particularly for someone planning to retire early.

Evaluating Withdrawal Rates and Spending

At 42 years old, the reader's desired withdrawal rate of 8.5% from a $2 million portfolio is unsustainable in the long term. This high withdrawal rate lacks a safety margin, especially considering the potential for market downturns and inflation. Alternatives include reducing annual spending, selling the business, or hiring a manager to alleviate daily operational burdens. Each option presents a pathway to reassess life goals and financial strategies.

The Bigger Picture

While money cannot guarantee happiness, it can provide comfort and reduce stress. The reader's situation highlights the importance of balancing financial goals with personal well-being. With no dependents and a significant asset base, taking time off to reflect on future endeavors may be a viable option. The conversation around covered call strategies and withdrawal rates serves as a reminder of the complexities involved in financial planning and the need for a holistic approach to retirement.

Why it matters

This article underscores the challenges of early retirement and the importance of understanding investment strategies like covered calls. As more individuals seek financial independence, grasping the nuances of withdrawal rates and income generation becomes crucial for sustainable financial health.

Get your personalized feed

Trace curates the best articles, videos, and discussions based on your interests and role. Stop doom-scrolling, start learning.

Try Trace free